AppLovin Stock Price Analysis. AppLovin (APP), a leading player in mobile technology, continues to gain traction with its innovative ad technology and strong market positioning.

As a company operating at the intersection of app development and mobile advertising, AppLovin’s dual approach positions it for robust growth in a competitive and rapidly expanding industry.

AppLovin YouTube Video Overview

1. AppLovin’s Business Model: Dual Segments Driving Success

AppLovin focuses on app discovery, marketing, and monetisation for mobile app developers. It operates through two primary segments:

- Software Platform: This includes a suite of tools leveraging artificial intelligence (AI), machine learning, and data analytics to optimise ad targeting and maximise developer revenues.

- App Portfolio: Owning a portfolio of mobile games allows AppLovin to test and enhance its software, creating a feedback loop that strengthens offerings for external customers.

This unique dual approach provides valuable insights and synergies, enabling the company to adapt quickly to market demands.

2. Expanding The Ad Tech Frontier

AppLovin’s reliance on AI and data-driven advertising solutions differentiates it in an increasingly complex digital advertising landscape.

Its AXON technology, for instance, optimises ad targeting, significantly improving returns for advertisers. This innovation, combined with its robust software platform, positions AppLovin as a leader in ad tech innovation.

Furthermore, strategic acquisitions, such as Adjust (a mobile analytics company), expand its capabilities, offering end-to-end solutions that span user acquisition, tracking, and monetisation.

3. Riding The Wave Of Market Growth

The global mobile gaming market is booming, driving demand for AppLovin’s user acquisition and monetisation services. The company’s platform capitalises on this trend, benefiting from the rapid expansion of app-based ecosystems.

In Q3 2024, AppLovin reported a 39% YoY revenue growth, fuelled by the success of its AI technology and the growing adoption of its ad platform.

4. Risks And Challenges

While AppLovin shows strong potential, several risks must be considered:

- Dependency on Digital Ad Spending: Economic downturns could lead to reduced ad budgets, impacting revenue.

- Regulatory Pressures: Privacy changes, such as Apple’s App Tracking Transparency (ATT), could limit user data tracking and reduce ad effectiveness.

- Intense Competition: Giants like Google, Facebook, Unity, and ironSource create a challenging landscape for AppLovin.

- Stock Volatility: As a relatively new public company, AppLovin’s stock may experience significant price swings.

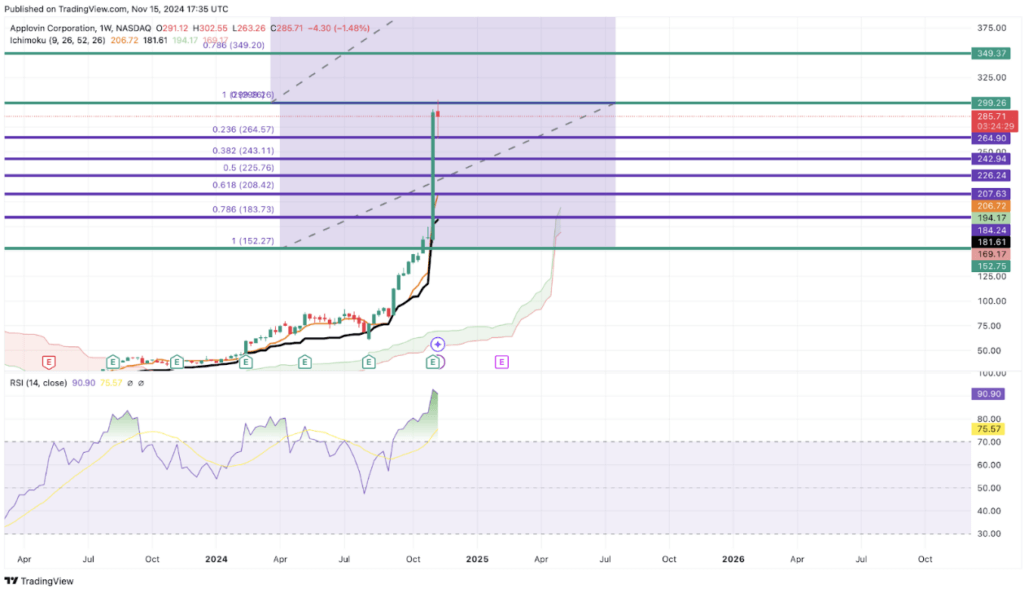

5. Technical Chart Analysis

In my analysis of AppLovin’s (APP) technical chart, I’ve identified three potential buy limit levels: $264.90, $242.94, and $226.24.

These levels represent price points where I believe favourable entry could be found, based on historical price action and key support areas. While AppLovin’s stock has experienced significant growth, I consider these levels as optimal points for those looking for a more favourable entry, particularly after recent price increases.

Despite the stock showing a steep uptrend and achieving a new resistance level of $291, the stock seems overvalued at the moment, with indicators like the RSI passing 80 suggesting potential near-term pullbacks. Given the current market conditions and bullish sentiment, my strategy is to initiate a position at the current market price (CMP) and layer in additional buy limit orders at the identified levels.

This approach allows me to capitalise on any price pullbacks and position myself for potential upside as AppLovin continues to expand in mobile advertising and gaming.

Remember: Investing is personal, and what works for me might not be right for you. Always conduct your own research and invest according to your unique financial goals and risk tolerance.

6. Is AppLovin Stock A Buy?

AppLovin’s strong revenue growth, high EBITDA margins, and robust free cash flow highlight its financial health. Coupled with its expanding ad tech capabilities and dual-segment strategy, the company is well-positioned for sustained growth.

For investors with a high-risk tolerance seeking exposure to mobile advertising and gaming, AppLovin presents a compelling opportunity.

However, given its current valuation, waiting for a pullback may offer a better risk-reward profile.

As always, conduct due diligence and align investments with your financial goals and risk tolerance.

Are You Ready To Learn How To Successfully Compound Your Investments?

Do you want to learn how to correctly analyse assets that suit your unique risk tolerance and financial goals?

Do you want to learn the powerful and proven 5 Step Invest Diva Diamond Analysis strategy as well as the Triple Compounding™ method I use, developed by my mentor, Invest Diva CEO, Kiana Danial?

Register for your FREE Triple Compounding™ Training HERE AND get Kiana’s Triple Compounding™ workbook and personal risk management toolkit for FREE.

If you liked my blog post about AppLovin Stock Price Analysis, you will love my blog post about ‘SiriusXM Stock Price Analysis‘

Disclosure: I am not a financial advisor and this is not financial advice. This information is for educational purposes only. This post ‘AppLovin Stock Price Analysis A Growth Stock Powering Innovation In Ad Tech And Gaming’ may contain affiliate links, meaning I get a commission if you decide to make a purchase through my links, at no cost to you. Please see terms of service page for more information.

Jes provides Premium Coaching Services for Invest Diva. This includes delivering live weekly coaching sessions and analysis for members of the Invest Diva Premium Investing Group. Jes is also a published author with Seeking Alpha.