Meta Platforms (NASDAQ: META) is no longer just a social media company, it’s become a global attention powerhouse. From Facebook and Instagram to WhatsApp and Threads, Meta is scaling engagement and weaving AI deeper into its business than ever before.

In Q2 2025, Meta posted a strong quarter with 22% year-over-year revenue growth, beating Wall Street expectations. It added 50 million new users since Q1, and average revenue per person reached $13.65. Still, investor sentiment is mixed. Shares jumped 12% after-hours, but some analysts remain cautious due to rising CapEx and signs of slower growth ahead.

The bigger story? Meta isn’t just gaining users, it’s making each one more valuable. AI-powered systems like Andrometa, GEM, and Lattice boosted ad conversions and raised average ad prices by 9%. More time spent on Facebook and Instagram (up 5% and 6%) turned directly into more impressions, conversions, and revenue.

Then there’s WhatsApp. Once tough to monetize, it’s becoming a quiet growth driver through paid messaging, Meta Verified, and AI tools, helping “Other Revenue” jump 50% year-over-year.

Meta’s edge lies in owning both the content and the algorithm. While Google depends on user searches, Meta uses behavior data to deliver hyper-relevant ads across its apps. With a founder-led vision and expanding AI infrastructure, Meta isn’t just leading today’s digital economy, it’s building for what’s next.

That said, risks remain. CapEx is projected to rise to $66 to 72 billion in 2025, with more spending on shorter-lived assets. That could pressure margins and free cash flow in the short term. But if Meta keeps delivering strong returns on investment, it’s well-positioned to grow faster than most peers.

So, is Meta’s long-term potential still underappreciated by the market? Let’s take a closer look using the IDDA Framework: Capital, Intentional, Fundamental, Sentimental, and Technical.

IDDA Point 1 & 2: Capital & Intentional

Before investing in Meta, ask yourself:

✅ Do you want exposure to a company that owns the full digital advertising funnel, from user behavior to ad placement to conversion?

✅ Are you looking to invest in a business that’s embedding AI into everything it does – from content delivery to monetization?

✅ Do you believe attention is the new oil, and Meta is building the pipelines?

Meta isn’t just experimenting with AI, it’s operationalizing it across every layer of its business. From building proprietary AI chips to overhauling its ad infrastructure, the company is methodically setting itself up to deliver hyper-personalized, high conversion ad experiences across Facebook, Instagram, WhatsApp, and Threads. Its strategy is intentional and long-term: maximize the value of every second users spend on its platforms by increasing both relevance and revenue per impression.

Capital wise, Meta is playing the long game. It’s allocating billions into AI data centers, augmented reality hardware, and next-gen infrastructure, not to chase hype, but to build the backend of tomorrow’s attention economy.

This approach also extends to ‘under the radar’ platforms like WhatsApp and Threads, which are now entering their monetization phase. Meta isn’t trying to be everything to everyone, it’s focusing on deepening value where it already dominates, and selectively scaling where it sees opportunity.

But it’s important to note: while Meta is a well established, highly profitable tech giant, its growth trajectory comes with volatility. As seen in 2022, Meta’s stock can experience sharp drawdowns during periods of market uncertainty or heavy investment cycles.

The company rebounded with strength, but such pullbacks may not suit all investors, especially those with lower risk tolerance or shorter time horizons. For long-term investors who believe in compounding digital infrastructure and AI monetization, Meta offers a compelling growth story. But for others, it’s a reminder that high-growth tech isn’t always a smooth ride.

Meta’s intentional reinvestment and focus on scalable, AI driven infrastructure make it one of the most strategically positioned companies in Big Tech but whether it fits into your portfolio depends on your conviction and your comfort with its market swings.

Don’t know your risk tolerance? Get Kiana Danial’s risk management toolkit for free here

IDDA Point 3: Fundamentals

🔹Meta delivered a strong Q2, with revenue rising 22% year-over-year to $47.52 billion, well above the expected range of $42.5 to $45.5 billion. The company also gave a solid Q3 forecast of $47.5 to $50.5 billion, pointing to continued growth of 17 to 24%. Average revenue per person reached $13.65 across 3.45 billion users, up by 50 million since Q1, showing strength in both user growth and monetization.

🔹A key reason for this performance is Meta’s investment in AI. Its recommendation systems boosted engagement, with time spent up 5% on Facebook and 6% on Instagram. Instagram video time jumped 20% year-over-year. Importantly, ad impressions increased without needing new ad spaces, showing that AI is helping get more value from existing platforms.

🔹This higher engagement translated into better monetization. Average ad prices rose 9%, thanks to improved targeting and Meta’s modular AI ad system – Andrometa, GEM, and Lattice – which boosted ad conversions by up to 5%. These tools help deliver more relevant ads and improve results for advertisers.

🔹Outside its core ad business, Meta is also growing new revenue streams. WhatsApp and Threads are gaining momentum, with WhatsApp’s AI features and paid messaging helping “Other Revenue” grow 50% year-over-year. Meta Verified subscriptions also contributed, showing strong potential for recurring income that’s still overlooked by many investors.

🔹Meta continues to manage its spending carefully. CapEx is expected to rise to $66 to 72 billion in 2025, focused mostly on AI infrastructure and short-term assets. While this could increase depreciation, operating costs remain under control. A recent change to server depreciation rules also helped keep reported expenses lower for now.

🔹Free cash flow margins have dipped slightly due to higher investment, but remain healthy. Meta’s strong returns on capital are helping it grow on a bigger scale. Even after the recent rally, its forward P/E ratio is still below the S&P 500 average, suggesting the stock may still offer good value given its growth potential and market leadership.

Fundamentals: Medium

IDDA Point 4: Sentimental

Strengths

✅ AI Is Delivering Real Results – Meta’s AI tools are boosting ad performance, with Instagram video time up 20% YoY and ad prices increasing 9%.

✅ Strong Growth in Revenue and Users – Q2 revenue grew 22% YoY, beating forecasts, and Meta added 50 million new users since Q1.

✅ Valuation Still Appealing – Despite strong growth, Meta trades below the S&P 500 on a forward P/E basis, leaving room for upside.

Risks

❌ Higher CapEx and Depreciation Ahead – Spending more on short-term assets will raise depreciation, which may squeeze margins and cash flow.

❌ Unpredictable Ad Spending – Ad budgets can shift quickly due to economic uncertainty or global events, affecting revenue.

❌ Growth May Slow – As Meta compares against a strong 2024, future growth rates may cool, which could affect investor sentiment.

Investor sentiment toward Meta has turned more positive after its strong Q2 results, which beat expectations despite earlier concerns about tariffs and ad spending. The stock jumped around 12% after hours, driven by solid growth, higher engagement, and early monetization progress on platforms like WhatsApp and Threads. Confidence is growing in Meta’s leadership and its practical use of AI, with CEO Mark Zuckerberg highlighting its long-term role in improving user experience. While some remain cautious about slower growth ahead as Meta compares against a strong 2024, the overall outlook is still bullish. Many investors now see Meta as undervalued given its ongoing progress in engagement, monetization, and disciplined spending.

Want our top stock picks and analysis every month? Get our monthly newsletter here.

Sentimental Risk: Medium – High

IDDA Point 5: Technical

On the weekly chart:

🟢 The Ichimoku Cloud remains green and wide, signaling strong bullish momentum and a sustained uptrend.

🟢 Price action is holding above the cloud, with the cloud itself acting as a dynamic support zone, reinforcing market confidence and suggesting potential for further upside as long as this structure holds.

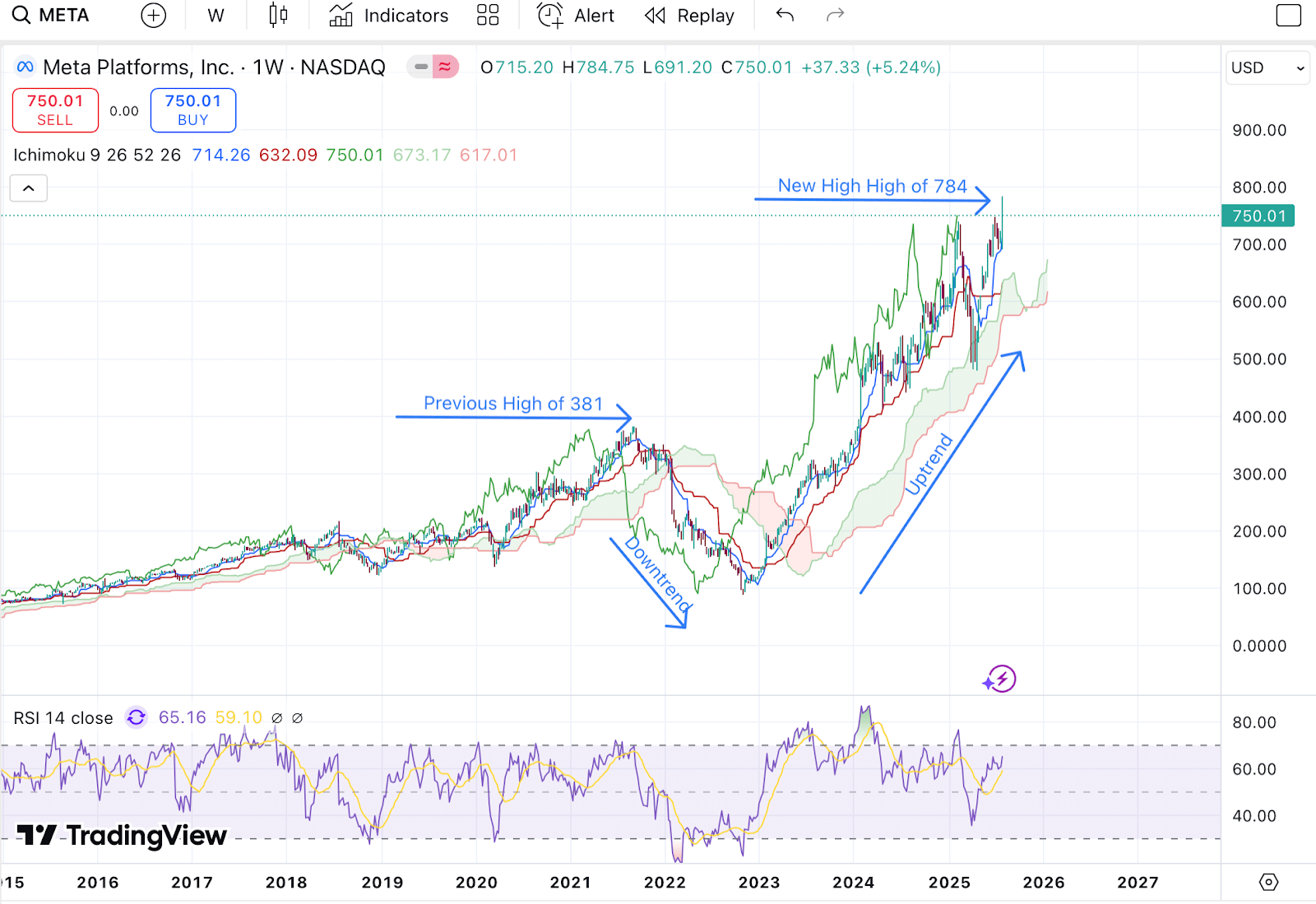

On the weekly chart, Meta’s sharp drop in 2022 was caused by heavy spending on the metaverse, weaker ad revenue, and a broader tech selloff due to rising interest rates. Apple’s iOS privacy changes hurt Meta’s ad targeting, while TikTok’s growth increased competition. Investors were also concerned about Mark Zuckerberg’s large investments in Reality Labs. As a result, the stock fell over 60% from its highs, despite still being profitable. Since then, Meta has bounced back in 2023 and 2024, breaking past its previous high of $381 and recently hitting a new all time high of $784 after strong Q2 earnings. The Ichimoku Cloud is bullish, with price action above the cloud, supporting the upward trend.

On the daily chart:

🟢 The Ichimoku Cloud is bullish, supporting the current uptrend and indicating continued positive momentum.

🟢 Candlesticks remain positioned above the cloud, reinforcing the strength of the trend and acting as a short-term support zone.

🔻 However, the RSI is currently in overbought territory, suggesting that a short-term pullback or consolidation may be on the horizon as the market cools off from recent gains.

On the daily chart, Meta pulled back at the start of 2025 after hitting a high of $739. The drop was mainly due to concerns over rising spending, especially on AI infrastructure and short-term assets, which raised fears about pressure on margins. Although revenue stayed strong, management warned that growth could slow compared to 2024’s high numbers. Combined with broader market caution, some investors took profits, leading to a healthy correction and potential buying opportunity.

After April, Meta began to recover as confidence returned. Investors saw stronger engagement, better ad performance, and growing revenue from WhatsApp and Threads. Momentum picked up further after Meta beat expectations in Q2 earnings, pushing the stock to a new high of $784 before showing signs of another short-term pullback.

Investors looking to get in META can consider these Buy Limit Entries:

📌Current market price 750 (High Risk – FOMO entry)

📌711.97 (High Risk)

📌667.27 (Medium Risk)

📌631.77 (Low Risk)

Investors looking to take profit can consider these Sell Limit Levels:

🎯783.75 (Short term)

🎯855.82 (Medium term)

🎯898.85 (Long term)

🎯Hold (Long term)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your

- CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: Medium

Meta (META) posted a strong Q2 FY25, with revenue growth and higher ad pricing fueled by increased engagement across Facebook, Instagram, WhatsApp, and Threads. Behind the scenes, AI tools like Andrometa, GEM, and Lattice are improving ad targeting and conversions, boosting ad prices without needing more screen time or ad space. “Other Revenue” also jumped 50% thanks to monetization gains from WhatsApp and Meta Verified subscriptions.

Final Thoughts on Meta (META)

While sentiment is turning bullish, one key advantage may still be overlooked: Meta’s modular AI ad system is quietly making its monetization more efficient. It allows Meta to grow revenue faster than user growth by getting more value out of existing engagement. Even though the stock popped around 12% after earnings, many analysts remain cautious due to rising CapEx and signs of slower growth ahead.

But unlike some AI hype stories, Meta is delivering real results. With strong fundamentals, growing cash flow, and multiple platforms now generating income, the recent high of $784 may not be the peak. Still, with overbought signals on the RSI, a short-term pullback could offer a smart entry point for long-term investors.

➡️ Key Takeaway: Buy the Dip or Opportunistic Accumulate

Meta’s long-term growth is underpinned by a monetization engine that’s getting smarter, not just bigger. For investors with a medium to high risk tolerance, short-term pullbacks could present a compelling entry point, especially if Meta’s AI advantage continues to fly under Wall Street’s radar.

Want to become a self sufficient Triple Compounder who no longer needs to read this blog?

Attend this free Triple Compounding Training here 👇👇

If you enjoyed my blog post about the ‘Meta Just Beat Earnings But This One AI Advantage Wall Street Might Be Overlooking Could Unlock Massive Upside’, you’ll love my post on ‘Apple (AAPL) Beat Earnings Expectations But This One AI & Innovation Disconnect Could Define Its Future (Or Not)’

Disclosure: I am not a financial advisor, and this is not financial advice. This information is for educational purposes only. This post about ‘Meta Just Beat Earnings But This One AI Advantage Wall Street Might Be Overlooking Could Unlock Massive Upside’ may contain affiliate links, meaning I get a commission if you decide to make a purchase through my links, at no cost to you. Please see the terms of service page for more information.

Grace provides Premium Coaching Services for Invest Diva. This includes delivering live weekly coaching sessions and analysis for members of the Invest Diva Premium Investing Group. Grace is a $100K Diva Award Winner | Entrepreneur, Investor & Content Creator. Starting from only $500 she built a six-figure portfolio with zero prior knowledge and experience using education from Invest Divas Triple Compounding Course.