SoundHound AI is a voice artificial intelligence company building conversational assistants that don’t just talk—they take action. Think ordering food, booking appointments, or helping drivers interact with their cars without touching a screen.

The company is making moves in the auto, restaurant, and enterprise space, with clients ranging from Hyundai and Kia to Allina Health and Peter Piper Pizza. It’s backed by NVIDIA and aiming to turn voice into the next major user interface.

The IDDA Analysis framework is used to analyze companies and determine which are right for you. There are five steps to the process:

- Capital Analysis – Your personal risk tolerance.

- Intentional Analysis – Your unique financial goals and timelines based on your age, health, and lifestyle.

- Fundamental Analysis – The viability of the asset based on company performance, financial health, and market position.

- Sentimental Analysis – The current emotions of Wall Street and other market participants.

- Technical Analysis – Historical price action to identify key psychological levels and market patterns.

Let’s dive into the IDDA analysis to assess SoundHound’s fundamental, sentimental, and technical outlook.

IDDA Point 1&2: Capital & Intentional

The capital and intentional analysis need to be conducted by you.

Select your assets in alignment with your financial goals. Listen to your intuition about each asset, but remember to invest based on your own values, not just because of recommendations from others.

Don’t know your risk tolerance? Get Kiana Danial’s risk management toolkit for free here.

IDDA Point 3: Fundamental

🔷 Revenue is growing fast

In Q1 2025, SoundHound posted revenue of $29.1 million. That’s a 151 percent jump compared to the same period last year. Their acquisition of Amelia and Allset is starting to pay off with more recurring revenue across enterprise and restaurant sectors.

🔷 Big-name partnerships keep stacking up

SoundHound works with Hyundai, Kia, Lucid, and now Tencent in China. They’ve also partnered with Peter Piper Pizza, Allina Health, and AVANT to roll out AI voice agents. These partnerships give them long-term revenue pipelines and brand credibility.

🔷 They’re going multi-industry

SoundHound is not just focused on cars. Their recent push into voice commerce and healthcare shows they’re building different income streams. That helps reduce risk if one sector slows down.

🔻 Still unprofitable and burning cash

Despite strong growth, SoundHound isn’t profitable yet. The company still burns cash, and margins remain thin. Until they scale further or improve cost efficiency, this could worry long-term investors.

🔻 Class-action lawsuit adds uncertainty

A securities fraud lawsuit is underway related to how the company accounted for its acquisitions. While it may not hit revenue directly, it could hurt investor trust or lead to fines or legal costs.

Fundamental Risk: Medium

The company has clear growth potential and strong partners but needs to show it can turn that into steady profits.

IDDA Point 4: Sentimental

Overall sentiment is cautiously bullish for SoundHound.

Strengths

✅ Analysts see potential in its unique voice-commerce model and enterprise expansion. The Amelia acquisition is expected to drive over $45 million in recurring revenue this year.

✅ The stock is backed by NVIDIA, which adds major credibility and investor excitement.

✅ Voice AI is a growing trend, and SoundHound is one of the few public companies offering a pure play in this space.

✅ Consumers are warming up to AI agents. A recent study shows 2 out of 3 would prefer to interact with a voice agent instead of a human.

Risks

❌ The stock has been highly volatile. Recent pullbacks show investors are still uncertain about profitability and long-term execution.

❌ A class-action lawsuit over accounting controls has raised red flags, especially for more risk-averse investors.

❌ Mixed analyst ratings. Some call it a buy while others see limited upside, especially with continued losses.

Sentimental Risk: Medium

Investors are excited about the tech and partnerships but still hesitant about financials and legal overhang. The optimism is there, but it’s cautious.

Want our top stock picks and analysis every month? Get our monthly newsletter here.

IDDA POINT 5 – TECHNICAL

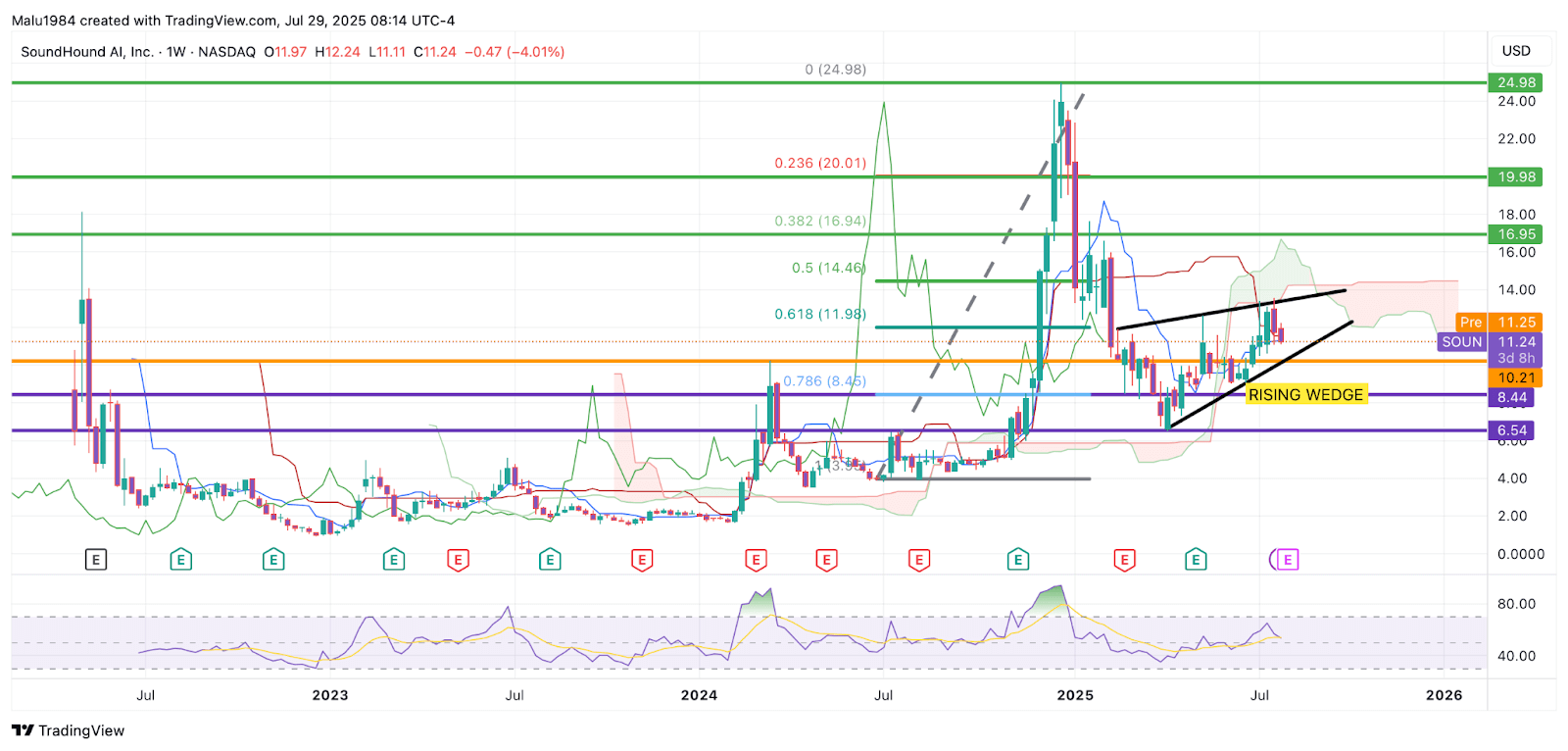

Weekly Chart:

🟢 Price is in an upward trend since April 2025

After falling hard from its December all-time high of $24.98 down to $6.54 in April, SoundHound has been climbing steadily.

🔻 Ichimoku Cloud is bearish

The cloud is red and wide. The price is still below it, showing strong resistance. The conversion line is also below the baseline, which confirms a bearish signal known as a dead cross.

🔻 Rising wedge is forming

The current upward move is shaping into a rising wedge pattern. That usually signals a bearish continuation, meaning another drop could be coming.

🔶 RSI is neutral

RSI sits at 53. That means the stock isn’t overbought or oversold. There’s no strong signal in either direction from this indicator.

🔶 High volatility

SoundHound tends to move fast in both directions. It’s a swing trader’s playground but not ideal for passive investors looking for calm price action.

Buy Limit (BL) levels:

📌 $10.21 – High Risk

📌 $8.44 – Moderate Risk

📌 $6.54 – Low Risk

Profit Taking (PT) levels:

📌 $16.95 – High Risk

📌 $19.98 – Moderate Risk

📌 $24.98 – Low Risk

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: High

The short-term uptrend looks promising, but the bearish cloud, dead cross, and rising wedge suggest caution. This setup could flip quickly if momentum fades.

Summary: Final Thoughts

SoundHound is an exciting but volatile stock sitting at the intersection of voice tech, AI, and commerce. On the surface, it looks like a voice assistant company. But when you dig deeper, three powerful growth drivers stand out.

First, the Allset acquisition isn’t just about ordering food. It’s a move into voice commerce, turning passive conversations into transactions across cars, TVs, and mobile devices. Second, SoundHound’s expanding footprint in the automotive world shows major trust from global car brands.

Their voice AI runs directly on NVIDIA hardware, giving them a tech advantage and long-term integration potential. Third, the Amelia acquisition gave them instant access to big enterprise clients and could unlock massive recurring revenue.

But not everything is smooth. The company is still unprofitable and under pressure to prove it can scale without burning cash. The class-action lawsuit also adds legal uncertainty and could weigh on investor confidence.

On the chart, the rising wedge and bearish Ichimoku signals suggest caution in the short term. The emotional tone around the stock is cautiously optimistic, but it’s fragile.

Overall Risk: Medium-High

SoundHound has the pieces for strong long-term growth but still faces execution risk. It’s a stock to watch closely—especially if you believe in the future of voice.

Want to become a self sufficient Triple Compounder who no longer needs to read this blog?

Attend this free Triple Compounding Training here 👇👇

If you enjoyed my blog post about SoundHound AI, you’ll love my post on What If the Next Quantum Leader Isn’t IBM or Google… But Rigetti Stock (RGTI)?

Disclosure: I am not a financial advisor, and this is not financial advice. This information is for educational purposes only. This post about SoundHound AI may contain affiliate links, meaning I get a commission if you decide to make a purchase through my links, at no cost to you. Please see the terms of service page for more information.

Invest Diva Premium Coach, $100K+ portfolio award winner, mom of 3. Increased family net worth from $200K in 2020 to $500K+ in 2024.