monday.com (NASDAQ: MNDY) is no longer just a project tracker, it’s becoming a full Work OS that brings work management, CRM, developer tools, and customer service into one platform.

This integration makes it harder to switch away and positions monday as a workflow “intelligence layer” for GenAI and automation. With CIOs cutting the number of software vendors they use, an all-in-one platform has real leverage, something the recent sell-off overshadowed.

Q2 was strong: fast revenue growth, very high gross margins, and a solid double digit operating margin. The company is cash rich, generating healthy free cash flow, and expects more for the full year. Growth is moving up-market, enterprise and CRM are expanding, while guidance calls for solid but slower growth as the company invests and adds senior leaders.

What the Street got wrong: the drop was driven by cautious near term guidance and sector wide multiple pressure, not a broken business. Vendor consolidation helps integrated suites, monday’s cross product expansion increases stickiness, and AI usage is surging across monday magic, vibe, and sidekick. Management expects meaningful AI revenue more in 2026 and onwards, but rising usage and deeper enterprise adoption point to a clear path from engagement to monetization.

Risks to watch: valuation is still premium vs. peers, net dollar retention ticked down, SMB demand softened after Google’s changes, billings are choppier, new CRM logos slowed as the mix shifts up market and near-term pricing upside is limited. Broader fears that agentic AI could reshape software/CRM economics also weigh on the sector.

So the big picture? A durable Work OS + AI roadmap facing near-term noise. Let’s map this using the IDDA (Capital, Intentional, Fundamental, Sentimental, Technical).

IDDA Point 1 & 2: Capital & Intentional

Before investing in MNDY, ask yourself:

✅ Do you want exposure to a consolidated Work OS spanning work management, CRM, dev, and service, benefiting from vendor consolidation and rising switching costs?

✅ Are you looking for a platform embedding AI into workflows (generation, assistance, automation) with usage scaling now and monetization likely from 2026 onwards?

✅ Do you believe high gross margins, growing FCF, and up-market enterprise wins can sustain growth through investment cycles?

Historically, high-growth software can swing hard and MNDY is down sharply in recent months. That volatility requires conviction and patience, but if you buy the Work OS + AI “intelligence layer” thesis, the long-term setup might outweigh the near-term noise. However, if volatility is not your cup of tea and you have a lower risk tolerance, then this stock may not fit your profile.

Don’t know your risk tolerance? Get Kiana Danial’s risk management toolkit for free here

IDDA Point 3: Fundamentals

🔹monday.com is moving from a basic project tracker to a full work operating system that brings together work management, CRM, developer tools, and customer service in one platform, making the suite more integrated and harder to replace.

🔹Their Q2 FY2025 delivered a strong quarter with fast growth, healthy margins, and plenty of cash. Free cash flow is rising, and growth is shifting up-market with more large enterprise customers, record retention, and a CRM business that’s now at meaningful scale.

🔹AI usage across monday magic, vibe, and sidekick is surging, with meaningful monetization expected from 2026 onward. Near term, management guides to steady but slightly slower growth as 2025 is an investment year (more hiring and higher R&D/GTMA spend).

🔹Key risks: a small dip in expansion from existing customers, softer SMB demand after Google search changes, choppier billings, slower new CRM logos as the mix tilts to enterprise, and limited pricing upside with much of the planned lift already accounted for.

Fundamental Risk: Medium

IDDA Point 4: Sentimental

Strengths

✅ Integrated suite + vendor consolidation: monday.com now spans work management, CRM, dev, and service in one platform, making it harder to rip out. With more CIOs consolidating vendors, this plays to its strengths; enterprise mix is rising and CRM has reached meaningful scale.

✅ Strong financials: Fast revenue growth, very high margins, a large cash cushion, and healthy, growing free cash flow point to a durable business that can keep investing while staying disciplined.

✅ AI momentum: Usage across monday magic, vibe, and sidekick is surging. Management expects real monetization to kick in from 2026 onwards, and many see the suite evolving into an AI enabled workflow “intelligence layer.”

Risks

❌ Premium valuation risk: Even after a pullback, shares trade richer than peers, making them vulnerable if growth softens or execution slips, and sensitive to sector wide multiple pressure.

❌ Near-term headwinds: Expansion from existing customers has cooled slightly; SMB demand softened after Google search changes; billings are choppier; new CRM logos slowed as the mix shifts up-market; and near-term pricing upside is limited with a good chunk already realized.

❌ Margin pressure in an investment year: Headcount is rising, and spending on product and go-to-market is higher. Guidance implies moderated growth and lower operating leverage near term while AI revenue hasn’t meaningfully arrived.

Investor sentiment is negative despite solid execution: the drop reflects cautious guidance, investment-driven margin pressure, and worries that AI agents could reshape software/CRM economics, while valuation, though lower, remains premium, leaving shares sensitive to hiccups.

Offsetting this, vendor consolidation favors integrated platforms like monday.com, some analysts have turned more positive on its “intelligence layer” potential, and many investors see the sell-off as overdone, others want clearer proof that enterprise wins keep compounding and AI usage turns into real revenue, likely a 2026-and-beyond story.

The bottom line: strong fundamentals and visible product momentum vs. high multiples and near-term noise, leaving the market split.

Want our top stock picks and analysis every month? Get our monthly newsletter here.

Sentimental Risk: High

IDDA Point 5: Technical

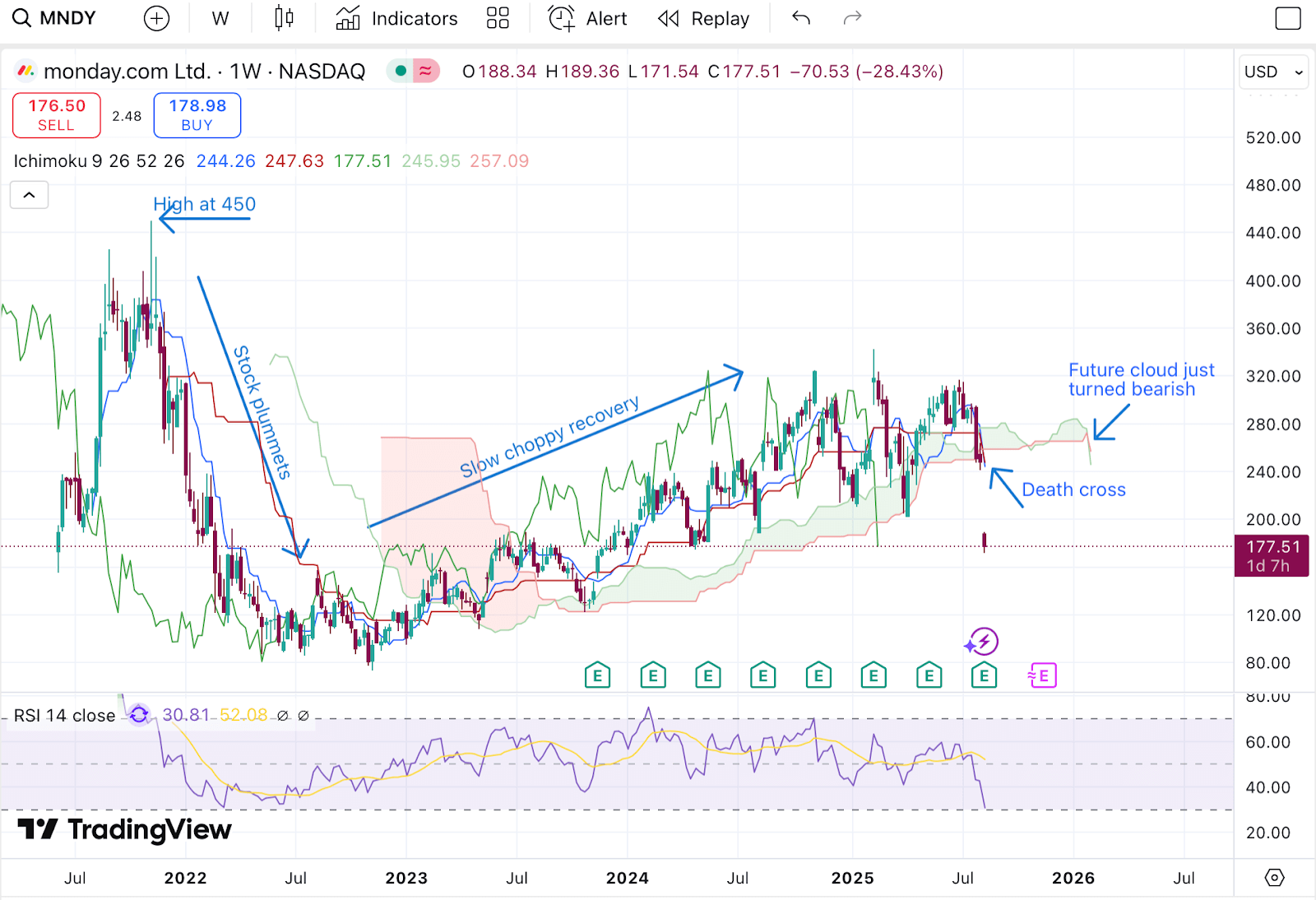

On the weekly chart:

🔻 The future cloud has turned bearish, marking the early start of a downward phase.

🔻 The latest candlesticks have dipped below the cloud, which now acts as a resistance zone.

🔻 The Tenkan line has crossed below the Kijun line (a “death cross”), reinforcing the bearish signal.

We can see on the weekly chart that in the early post-IPO phase the stock climbed to about 450 in November 2021, then fell sharply in December 2021. Since then, it has been slowly recovering with significant pullbacks – some around 50%, others up to 78%, and has struggled to reclaim prior highs. After the recent drop, the latest weekly candle sits below the cloud (now acting as a resistance zone), and the Tenkan has crossed below the Kijun, reinforcing the bearish setup.

On the daily chart:

🔻 Like the weekly chart, the forward cloud is bearish and a death cross is in place, signaling a downward phase.

🔻 Price has fallen well below the cloud, which now acts as a resistance zone.

🔻 RSI is oversold at 19.19, hinting at a possible near term reversal (though any bounce would be counter-trend).

On the daily chart, the forward cloud is firmly bearish and a clear death cross confirms a downward momentum, signaling that the path of least resistance remains lower. The latest candlesticks have fallen well below the cloud, which now acts as a resistance zone. At the same time, RSI is deeply oversold at 19.19, which can trigger a reflex rebound. The current market price has retraced to as far as 61% on the Fibonacci retracement level.

Investors looking to get in MNDY can consider these Buy Limit Entries:

📌Current market price 175.83 (High Risk)

📌131.21 (Medium Risk)

📌73.71 (Low Risk)

Investors looking to take profit can consider these Sell Limit Levels:

🎯240.30 (Short term)

🎯279.27 (Medium term)

🎯342.39 (Long term)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: High

Final Thoughts on monday.com (MNDY)

monday.com isn’t just a project tool anymore, it’s evolving into a full Work OS that unifies work management, CRM, developer tools, and service into one integrated platform.

The recent crash was largely about cautious near-term guidance and sector-wide multiple compression, not a broken business. In a market where CIOs are actively consolidating vendors, a single platform that organizes work, data, and cross-team processes carries real strategic weight, yet that long-term shift got lost in the sell-off.

What the Street may have missed is the focus stayed on the next quarter instead of the trajectory. Enterprise and CRM momentum continue to build, retention remains strong, and AI usage is surging across monday magic, vibe, and sidekick.

Management is clear that significant AI monetization is a 2026-and-beyond story, but the usage signals and up-market mix today point to a credible path from engagement to revenue tomorrow. Add a healthy balance sheet and consistent free-cash-flow generation, and the company has ample firepower to keep investing through the cycle.

Risks to still consider are the valuation still sits at a premium to peers, leaving the stock sensitive to any growth wobble, expansion from existing customers has cooled a touch, SMB demand has been softer, billings can be choppy and pricing levers near term are limited.

However the bigger picture is investor nerves around agentic AI reshaping software/CRM economics can keep pressure on the group’s multiples.

The weekly and daily trends lean bearish with price below the cloud and a recent “death cross,” signaling that the path of least resistance is down until the structure repairs. At the same time, as RSI is oversold, so sharp counter-trend bounces are possible in the short term but they need to follow through back toward the cloud to flip the setup from relief to repair.

➡️ Key Takeaways: Accumulate on weakness with a long-term horizon – or take profits on strength if your timeline is shorter.

If you believe in the Work OS + AI “intelligence layer” thesis, consider selective buying on pullbacks and steady, patient accumulation aligned with your risk tolerance. For investors looking to take short term profit, the stock’s volatility can also offer swing-trading opportunities.

Want to become a self sufficient Triple Compounder who no longer needs to read this blog?

Attend this free Triple Compounding Training here 👇👇

Register FREE Now! Get Your Risk Management Toolkit And Workbook FREE When You Attend

If you enjoyed my blog post about ‘MNDY Stock: The Truth Behind the Crash & What the Street Got Wrong’, you’ll love my post on ‘ASML Stock: Why the World’s Only EUV Maker Could Be Wall Street’s Biggest Blind Spot’

Disclosure: I am not a financial advisor, and this is not financial advice. This information is for educational purposes only. This post about ‘MNDY Stock: The Truth Behind the Crash & What the Street Got Wrong’ may contain affiliate links, meaning I get a commission if you decide to make a purchase through my links, at no cost to you. Please see the terms of service page for more information.

Grace provides Premium Coaching Services for Invest Diva. This includes delivering live weekly coaching sessions and analysis for members of the Invest Diva Premium Investing Group. Grace is a $100K Diva Award Winner | Entrepreneur, Investor & Content Creator. Starting from only $500 she built a six-figure portfolio with zero prior knowledge and experience using education from Invest Divas Triple Compounding Course.